July's Market Insights

Political certainty and potential rate drop bode well for Autumn market

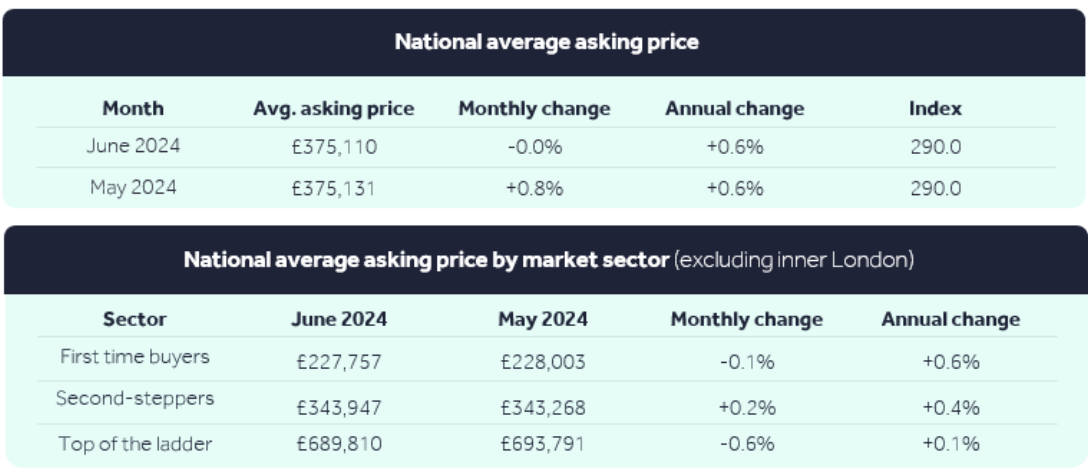

- Average new seller asking prices drop by 0.4% (-£1,617) this month to £373,493, a bigger July drop than usual, as new sellers try to cut through the distractions of the General Election, sporting events and summer holiday season with a tempting price

- Market activity has remained steady throughout the General Election campaign, and though there are signs that some would-be movers are waiting for the first Bank of England Base Rate cut, most are continuing with their moving plans:

- The number of sales being agreed remains encouraging at 15% above the same period a year ago, when mortgage rates were approaching their peak

- The number of new sellers coming to market is a steady 3% above last year

- Buyer demand remains stable overall, but there’s a slight drop (-2%) in demand in the particularly affordability-stretched first-time buyer sector

- Current market expectations are that the first Bank of England Base Rate cut may be as soon as August or September, which would be a boost for most home-movers and bodes well for the Autumn market:

- The average five-year fixed rate is now 4.97%, which while below the peak of 6.11% in July 2023, is still much higher than the average of 2.51% in July 2021, before the first of 14 consecutive rate increases

The average price of property coming to the market for sale drops 0.4% (-£1,617) to £373,493. This is a bigger drop than the 20-year July average of -0.2%, as sellers try to capture the attention of buyers with a more tempting price heading into the thick of the summer holidays and the Olympics. Home-movers are dealing with more diversions than normal at this time of year, having just come through the distractions of the General Election campaign and the Euro football tournament, but prices remain stable overall at 0.4% higher than a year ago.

Despite concern among some that the General Election campaign would lead to a significant slowdown in home-moving activity, Rightmove’s millions of data points show that the vast majority of people have been getting on with their moves since the election was called. The political certainty of having the next government in place is likely to aid home-mover confidence heading into the second half of the year. What is still outstanding and of more pressing concern to home-buyers is when the first interest rate cut will be, with persistently high mortgage rates continuing to test affordability.

“Three major uncertainties hanging over the property market at the start of the year were when the first interest rate cut would be, and the timing and the result of the General Election. We’ve now got the political certainty of a new government with a large majority, which we expect will help home-mover confidence. It’s very early days, but the new Chancellor’s immediate announcements on housebuilding targets and planning reform are positive signs that the government is keen to get going with its manifesto pledges. With many areas of the market that could be improved, we hope that the new government is able to get on with its plans and deliver sustainable housing policies that help the market in the medium to longer-term. One area of the market in need of more support is first-time buyers, many of whom have been stretched to the limit by high mortgage rates, with some also facing higher stamp duty fees when the current thresholds are set to revert in March 2025.”

Tim Bannister Rightmove’s Director of Property Science

The number of sales being agreed is now an encouraging 15% above the same period a year ago, when we were approaching the peak of mortgage rates. This compares to last month’s figure which was +6% above last year. This positive sales figure emphasises that serious home-hunters have been largely undeterred by the General Election and have been getting on with their moves. Similarly, the number of new sellers coming to market in the last four weeks is a steady 3% above last year, indicating that despite the uncertainty of an election, the vast majority of movers haven’t been put off.

A key concern for many home-movers is when the first Bank of England Base Rate cut will be, and there are signs that some pockets of movers are waiting for this before acting. Overall buyer demand, measured by the number of would-be buyers contacting estate agents about homes for sale, has remained stable in the last four weeks when compared with this time last year. However, there’s a slight drop (-2%) in buyer demand in the particularly affordability-stretched first-time buyer sector, as some look to rate cuts to improve their affordability.

Some good news for home-movers is that the financial markets expect that the first Base Rate cut will be in August or September. Though this expectation could change over the coming weeks, it would be a boost for home-movers and market sentiment leading into Autumn. Rightmove’s weekly mortgage tracker shows that the average five-year fixed rate is now 4.97%, which while improved from the peak of 6.11% in July 2023, is still much higher than the average of 2.51% in July 2021, before the first of 14 consecutive Base Rate increases. Political certainty and a first rate cut for four years could together set the backdrop for a positive Autumn market.

“A Base Rate cut is expected to lead to lower mortgage rates, which could be the gamechanger for some would-be home-movers who are being held back by significantly higher monthly mortgage costs. The average five-year fixed rate is still nearly twice as high as it was before the first of 14 consecutive Bank of England rate increases in 2021, with rates staying elevated for much longer than many thought that they would. A first Base Rate cut for over four years, together with the new political certainty, could set the scene for a positive Autumn market, with improved affordability and a more confident outlook in the second half of the year.”

Tim Bannister Rightmove’s Director of Property Science

July's Market Insights

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024